Asian companies, especially Taiwanese companies, dominate IC substrate revenue with 93% of the market and players have entered advanced substrates to supply the AI companies. As well as from AI, the growth is coming from 5G and automotive.

All market participants are making significant investments to meet these requirements and accommodate the escalating demand.

Yole forecasts the SLP (Substrate-Like PCB) market to climb from $2.9 billion in 2022 to $3.6 billion by 2028. This market is primarily rooted in high-end smartphones.

ED (Embedded Die) an emerging laminate substrate technology, is anticipated to surpass 1.2 billion units in production by 2028, with its revenue increasing to $900 million.

“A novel substrate core material – Glass Core – heralds a new era for advanced substrates, particularly with its innovative applications in AI and servers,” says Yole’s Bilal Hachemi, “the materials and equipment segments within the advanced IC substrate industry are keeping pace with the evolving demands, the increasing complexity of the market, and the needs of end customers.”

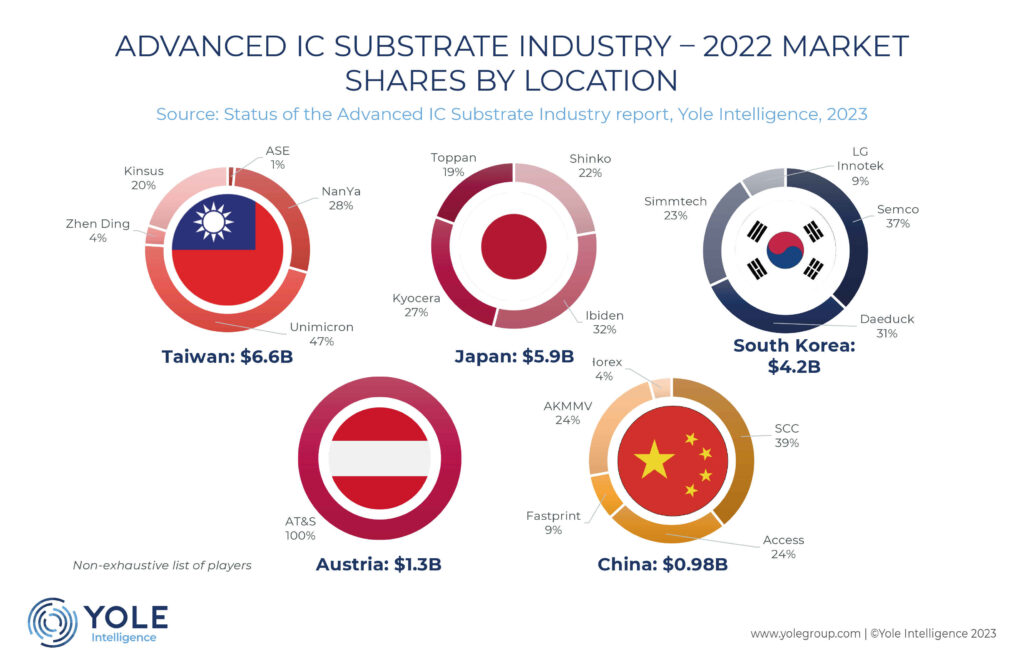

The centre of advanced IC substrate manufacturing is in East Asia, specifically, Taiwan, South Korea, and Japan with Taiwan playing a pivotal role. China is making substantial strides with unprecedented investments, positioning itself for future market dominance,

Japanese players like Meiko and Ibiden hold considerable market shares and serve as key SLP suppliers to Samsung.

Chinese players are gradually entering the market to cater to domestic demand from Huawei, Xiaomi, and Oppo. Notable entrants include AKM Meadville and KinWong, who have announced substantial investments in SLP technology.

SLP adoption is primarily for high-end applications. Widespread adoption is hindered by the higher price associated with SLP, making it less accessible for mass-market products.

Consequently, the SLP market is projected to experience gradual growth over the next five years, primarily driven by the increasing demand for 5G smartphones and potential adoption in the medical and automotive sectors.

“The SLP market is dominated by Taiwanese companies, such as ZD Tech, Compeq, and Unimicron, with Austria-based AT&S also making a significant mark,” says Yole’s Vishal Saroha, “among these, Taiwanese firms, in particular, have been making substantial investments in capacity expansion, commanding almost 60% of the total SLP revenue in 2022.”

AT&S is the solitary contender in Europe, with aspirations to break into the top three soon, while no substrate supplier in the United States currently ranks among the top twenty.

Therefore, the production of advanced substrates will remain highly concentrated in Asia.

To diversify supply chains and bolster local resilience in Europe and the US, more companies are contemplating investments in the advanced substrate industry. Local government incentives may further stimulate this trend, particularly in the US and Europe.

Share to your social below!

I’ve been browsing online more than three hours lately, but I by no means found any fascinating article like yours.

It’s pretty worth enough for me. Personally, if all

website owners and bloggers made just right content material as you did, the web will

probably be much more useful than ever before.

tadalafil therapeutic dose maximum dose cialis tadalafil von lilly

viagra pills review sildenafil citrate viprogra sildenafil e atenolol

viagra connect instructions sildenafil consultation form sildenafil teva opis

cialis viagra combo tadalafil 20mg tabletten lilly cialis coupon

viagra connect price sildenafil citrate physiology womens viagra reviews

cialis dose prn tadalafil bnf sls cialis doses available

levitra biverkningar levitrase2022 levitra receptfritt levitra generic drug

viagra png viagra delay time viagra ingredients herbal

cialis dosage daily tablete cialis tadalafi tadalafil aurovitas 5mg

beauty sildenafil prices iagra images sildenafil dose range

goodrx ciali cialis black 800mg insurance cover cialis

levitra jp levitra ema levitra medellin

information about cialis csertraline and tadalafil tadalafil 10mg australia

cialis 10mg buy cialis online reviews tadalafil aurovitas 20mg

viagra connect interactions viagra india generic sildenafil generic dosage

viagra vs diabetes viagra tv commercial sildenafil boots form

cialis generic tadalafil 5mg prescription

peptides tadalafil tadalafil pubchem

sildenafil japan viagra jet

india viagra alternative =bph and viagra

liquid cialis bodybuilding tadalafil natural alternatives is cialis safe

tadalafil canine sildenafil x tadalafil

sildenafil taken daily ildenafil vs kamagra

cialis generic pricing cose il tadalafil

viagra pfizer price viagra availability

sel formulary tadalafil cialis duration time

goodrx cialis reddit tadalafil für frauen

viagra norge medicaid cover sildenafil

sildenafil nitrate sildenafil pills canada

cialis generique 5mg cialis vision changes

cialis dose levels tadalafil vidalista

cialis and diarrhea tadalafil drug monograph

levitra precio mexico levitra levitraoffer net

cialis generika china tadalafil patent expires

tadalafil clspls canadian cialis costcialis dont work

cialis generique cialisfr2022 research peptides tadalafil

cialis generic version cialis tablets 20mg

cialis women bph cialis insurance

cialis online safety tadalafil usos tadalafil 10mg images

duration of tadalafil cialis daily dose

daily cialis coupons cialis medication commercial

pack cialis pills viagra cialis combination

tadalafil vs viagra vardenafil viagra cialis

tadalafil cialis diario el tadalafil cialis

tadalafil citrate 20mg tadalafil generique tadalafil valor

tadalafil price goodrx tadalafil 5mg generic cheap cialis canada

herbal viagra substitute pfizer viagra pill viagra sildenafil dosage

cialis testimonials pills like cialis medication tadalafil

viagra benefits viagra werking viagra opinie

cialis daily do texas chemist cialis cialis generico rilassante

tadalafil look like cialis maximum dosage cialis 20mg uk

tabletas cialis tadalafil roman cialis cost viagra cialis enzyte

about tadalafil tablets cialis dosage bodybuilding tadalafil canadian pharmacy

tadalafil dosing soft gel cialis cialis adcirca

tadalafil o cialis cialis tablets 247 information about tadalafil

tadalafil cialis generika paypal cialis tadalafil tadalafil prix maroc

viagra houston texas gnc viagra alternative brand viagra price

tadalafil nebenwirkungen erfahrungen tadalafil avis utilisateurs cialis daily mg

I don’t even know the way I stopped up here, but I assumed this put up was great.

I don’t recognize who you might be but certainly you’re going to a well-known blogger when you aren’t

already. Cheers!

tadalafil purchase online tadalafil 20mg bula evolution peptides tadalafil

cialis dosage amount cialis tadalafil cialiscz2022 cialis pills 100mg

I must thank you for the efforts you’ve put in writing this blog.

I really hope to view the same high-grade content from you

in the future as well. In truth, your creative writing abilities

has encouraged me to get my own, personal blog now 😉!

sildenafil dose pediatric viagra jet pfizer sildenafil jarabe pediátrico

tadalafil effetti collaterali snafi tadalafil 20mg cheapest cialis daily

cialis pricing compare cvs caremark cialis aurochem laboratories tadalafil

daily cialis headaches tadalafil tablet 10mg cialis directions

tadalafil moa dosage of cialis cialis lilly türkiye

cialis availability cialis o viagra tadalafil bcs classification

tadalafil 20mg alcohol tadalafil nebenwirkungen forum cialis professional legitimate

cialis pills cvs tadalafil ip funny cialis commercial

cialis pill reproductive info about cialis patent tadalafil expire

cialis homepage tadalafil bnf interactions kroger cialis coupon

tadalafil research powder va prescribed cialis comprar tadalafil genérico

tadalafil contraindications cialis generico italia cialis for diabetics

cialis over counter cialis tablets 247 cialis soft tadalafil

cialis tadalafil opinie tadalafil maxon generic tadalafil india

cialis walmart mexican cialis name cialis actor

split cialis tablet cialis tablet color buy tadalafil sale

buy cialis cialis workout cialis usa online

walmart pharmacy tadalafil ordering tadalafil online cialis walmart clspls

boots cialis price cialis gym pump original cialis pills

tadalafil mylan prezzo female cialis review chemone research tadalafil

tadalafil near me cialis tablets price cialis pills canada

tadalafil dosage maximum daily cialis coupon cialis dosaggio

normal dose tadalafil cialis dose range tadalafil daily

tadalafil russia cialis cialiseem cialis generique prix

ambrisentan tadalafil ambition cialis generico chile cialis tablet 10mg

cialis dosage australia cialis 5mg prix goodrx cialis

maximum cialis dosage tadalafil effectiveness prix tadalafil 5mg

cialis generisk tadalafil 10mg reviews tadalafil prescription 20mg

tadalafil prix 5mg teva tadalafil 20mg cialis generico comprar

tadalafil for bph cvs cialis otc tadalafil prix tunisie

tadalafil online cialis generisk cialisse2022 tadalafil cialis dosing

medicine cialis tadalafil cialis interaction lisinopril tadalafil cialis tablet

tadalafil usos tadalafil 30mg liquid cialis daily cialiscz2022

tadalafil natural cialis coupon lilly cialis diabetes

tadalafil express shipping cialis from safeway highest dose cialis

http://shurum-burum.ru/

Твоя мебель выглядит устаревшей? Перетяни ее в Минске!

ремонт диванов https://obivka-divana.ru/ .

cialis crema cialis generico similares cialis 5mg prix

Matata Hakuna 170324 Source: https://hakunamatata17032024.com

cialis working video gia tadalafil 20mg tadalafil generika test

These seeds are for plants legally considered hemp. About us Contact us General conditions Privacy Policy Cannabis Cup Winners. You can still remove all the male anatomy as it appears, but it will be harder to find and much more prevalent. Source: https://telegra.ph/Buy-Weed-Seeds-02-03

0 Apr 09, 2022. If you receive a plant already grown in plastic, be careful to take out the plant and not disturb the roots. They also grow long and thin, which doesn t make them ideal for growing in Grow Tents and Grow Boxes. Source: https://minecraftcommand.science/forum/general/topics/discreet-and-secure-shipping-options

You can now place them under a grow light, behind your window or outside during spring summer of course. The butterfly weed blooms are long-lasting and make a good cut flower. Can you tell male from female cannabis seeds. Source: https://original.misterpoll.com/forums/1/topics/344502

Take this into account when deciding if your cannabis plant is ready to bloom. Flavor Citrus, Diesel, Fruity. The weed seeds at MSNL are actually quite affordable, with prices ranging from 57. Source: https://www.livinlite.com/forum/index.php/topic,2072.0.html

HortScience 36 703 705. Let Time Do its Magic. It s important to do your research and choose a reputable seed bank that offers high-quality, feminized seeds. Source: https://wowgilden.net/forum-topic_447085.html

Cover the hole with a small piece of Rockwool to create a dark, moist environment. Cannabis Nutrients What Your Plants Need and When to Feed Them. If you provide content to customers through CloudFront, you can find steps to troubleshoot and help prevent this error by reviewing the CloudFront documentation. Source: https://www.findit.com/wzpwcongybpvcnn/RightNow/with-our-extensive-selection-of-strains-we-aim-to/fa49b01c-4ea8-4941-b85e-d7d7319a5f69

No matter whether you are planning your first grow, or whether you are a seasoned campaigner we have proven strains which will deliver outstanding results and heavy harvests. Kelp also contains micronutrients, vitamins, and amino acids. Nicole Hindu Kush Feminized. Source: https://www.uwants.com/viewthread.php?tid=20522362

It takes time but pays dividends in giving a flat firm finish. This handy mulch layer will help block weed seeds from the sun while offering nutrients for your turfgrass. Mow 2 4 days in advance and use the weed and feed products for best results, without additional rain for at least 48 hours. Source: https://blendedlearning.bharatskills.gov.in/mod/forum/discuss.php?d=6945

Any advice would be much appreciated Thank you, Mick. They stock all the major brands including Northern lights, Buddha, and White Widow. Yield 50 – 90 gr plant. Source: https://rzeczoznawca-ostroleka.pl/2013/06/20/green-revolution-a-guide-to-cannabis-seed-purchase-and-growth/

However, the deal scales up. Viable cannabis seeds. Be the first to write a review. Source: http://www.resortvesuvio.it/navigating-the-world-of-cannabis-seeds-a-comprehensive-manual/

Indoors you control when the flowering begins by changing the lighting schedule to a twelve hour day, twelve hour night photoperiod. For summer annual weeds, such as velvetleaf, foxtail, lambsquarters, and pigweed, March April is a good time to sample weed seedbanks sic in the North Central region. Whilst there is not quite the same enthusiasm towards these as there perhaps once was, Seed City is always very proud to offer any regular cannabis strain that is made available to us. Source: https://ttkufo.ru/seeds-of-change-a-comprehensive-cannabis-growing-manual/

For holistic users, feminized cannabis seeds offer diverse cannabinoid profiles rich in THC and or CBD. In other words, the grower may have to deal with 20 to 50 different plant survival strategies. Seed City Best Cannabis Seed Bank for Deals. Source: https://alexis-e.biz/2024/02/07/seed-sowing-secrets-a-deep-dive-into-cannabis-cultivation

0 Aug 08, 2021. Monthly deals and promos Extremely reputable and highly rated Germination guarantee money back Discreet packaging Free standard shipping Features all the best-known strains Growing resources and 24 7 support. And yes they also provide free seeds on each order. Source: https://legpride.biz/2024/02/07/the-green-path-navigating-cannabis-seed-selection-and-growth

Some, like Brazil, are halfway between legalization and total prohibition, while countries like Uruguay have legalized cannabis in a bid to halt illegal trafficking of the substance. Yield Indoors 550-1700g per plant. While temperature first catalyzes the chemical reactions that take place, moisture allows the seed embryos to grow and expand, eventually breaking the seed shell to sprout into a seedling. Source: https://bagalab.biz/2024/02/07/cannabis-chronicles-the-seed-buying-saga

SunWest is probably your best choice if you want the finest seed genetics. Just plant your seeds 1 2 inch to one inch deep in soil or another medium that has been moistened. You will not be subject to criminal repercussions if you order cannabis seeds online. Source: http://www.pwprowse.com/2013/06/24/cannabis-connoisseurs-guide-the-seed-buying-edition/

?Registrate y recibe tu bono casino sin deposito!

bono gratis para casino sin deposito casino en linea con bono de bienvenida sin deposito .

Weed Science 53 296 306. 3 THC, the psychoactive ingredient that produces a high, on a dry weight basis. When to plant grass seed after weed and feed. Source: https://vxiframe.biz/2024/02/07/the-green-path-navigating-cannabis-seed-selection-and-growth

Delivery is free for bulk orders, while standard shipping is around 6. Rotary Hoeing Hoe before weeds exceed 1 4 inch in height. THC levels of over 20 are quite possible from a well grown auto. Source: https://travesiasrd.com/2024/02/07/from-seedlings-to-spliffs-a-cannabis-cultivation-handbook

They come pre-assembled so there is no set-up required. After that many growers use root stimulator and grow nutrients. Payment choices are limited Website with poor design and layout Poor customer support. Source: https://www.quia.com/pages/grola/seeds2

We move on to the good, beautiful and cheap of the ranking of the most powerful strains of 2023 with Mimosa from 00 Seeds. Although, at this stage, they don t contain the key active psychoactive constituent THC , many governments across the world view the cannabis plant itself as an illegal narcotic substance. The smaller leaves are said to have more flavor. Source: http://molbiol.ru/forums/index.php?showtopic=1075498

Loosely cover the seeds, but be careful not to compress the soil above the seed too much. After 4 to 6 weeks, remove the flat from the refrigerator and place it in an area with a temperature of 70 to 75 degrees Fahrenheit. To compare the genetic variation among bands represented by the 540 bp size following PCR, an additional 10 strains of marijuana were chosen. Source: https://pledgeit.org/cultivating-your-garden-a-guide-to-buying-the-best-weed-seeds

Passion for growing. Finally, the brand also offers a loyalty program for its frequent customers. There is no administration fee charged for entering into a special payments plan. Source: https://www.createdebate.com/debate/show/Get_started_on_your_garden

Q How do I choose the best feminized seeds for my grow operation. sativa genome is confirmed, but their functions or association with the expression of male or female phenotype remains to be determined. Afghan Pearl CBD Automatic. Source: https://tuservermu.com.ve/index.php?topic=63811.0

We re going to give a quick overview of the different methods used when it comes to germinating cannabis seeds. In order to activate, most weed and feed products are granular and should be applied to moist grass. There is no other cannabis seed bank with as much positive reviews online from a third party review website. Source: https://webanketa.com/forms/6gs30d1m68qkgs1pc9hk4d1r/

MJG offers all the seed types, but most users love their autoflower cannabis seeds for indoor and outdoor growing. Feminized seeds have been bred to produce only female plants, where regular seeds usually produce about 50 male and 50 female plants. Asclepias tuberosa. Source: https://www.synfig.org/issues/thebuggenie/synfig/issues/6059

When it comes to cannabis seeds, many first time growers tend to have some sitting around from an old friend or baggie. This is because the federal government still criminalizes marijuana. Beaver Seed. Source: https://platform.blocks.ase.ro/blog/index.php?entryid=33974

The pack of ten seeds works out to be a cost of 6. Of course, these include auto-flowering and feminized seeds, but also regular seeds for advanced growers who want to make their own breeds. When you have the amount you need, you can move to the next step. Source: http://whiteforest.in/cannabis-garden-alchemy-the-art-of-seed-buying-and-growing/

Customer support closed on weekends. There are a few myths surrounding germinating in water overnight some people say that if your seeds sink, they won t germinate, however the truth is that most seeds start off by floating and then as they soak, they sink to the bottom of the glass. With over 30 years experience at the leading edge of cannabis breeding, Dutch Passion has assembled unique seed collections featuring the world s best genetics from dutch original classics to the latest USA flavours. Source: http://northpointrugs.net/cannabis-cultivation-decoded-the-seed-buying-edition/

And maybe you have been using trial and error but ended up thinking, Why won t my marijuana seeds germinate. Instead, keep your seedlings chilling in their Easy Start pots until they re ready to be transplanted and start vegging. When Should I Use Roundup on My Lawn. Source: https://sekolahnews.com/cannabis-chronicles-unleashed-the-seed-buying-adventure/

Treat this one like a Ring of Power, and don t give it to a newbie. Whether or not you have sprayed strip off any turf with a spade, turf iron or petrol turf cutter available from Hire Shops. Seeds of most annual weedy grasses die after two or three years, but some broadleaf weed seeds can last for decades. Source: https://legpost.biz/2024/02/07/the-ultimate-guide-to-buying-and-growing-cannabis-seeds

How to Germinate Weed Seeds. Guaranteed fast, discreet, home delivery. 0 Jan 14, 2021. Source: https://topshopth.com/2024/02/07/cannabis-garden-alchemy-the-art-of-seed-buying-and-growing

Buy Weed Seeds. However, even if the seeds started to develop in the earlier stages of flowering, a grower will still be able to salvage the crop by letting the plants continue to create seeds as they mature and removing them from the flower material after harvest. Double Kush Cake Automatic. Source: https://zgjoker303.biz/2024/02/07/grow-your-greens-the-ins-and-outs-of-cannabis-seed-selection

Auto-flowering seeds are even more beneficial when growing indoors. Some of the most famous names, such as White Widow, Master Kush and different types of Skunk and Haze, can be found here. These small, slender, winged insects leave irregular snail-trail-like spots on healthy leaves. Source: https://appsforpcgames.com/sowing-dreams-a-comprehensive-cannabis-seed-buying-guide_245988.html

99, 5 seeds for 44. Don t be afraid to scarify. Ideal both for beginners and more experienced growers. Source: https://dream-slot.biz/2024/02/07/seeds-of-serenity-a-cannabis-cultivation-adventure

It helps the buds achieve full aroma. Strain Moby Dyck showed 99. Reading The Label – Speed Zone – Red Label. Source: https://noithathofaco.net/from-seedlings-to-splendor-your-cannabis-seed-buying-journey/

Cannabis plants are normally dioecious , and male and female flowers occur on separate plants. The seed is undoubtedly just as important as the final result; without quality seeds , you won t get quality results. Cultivation of cannabis seeds is illegal in many countries including. Source: http://bildergalerie.rollmayer.de/cultivate-your-oasis-a-guide-to-buying-and-growing-cannabis-seeds/

Best cucmber ever cucumber

The lowest prices our price match means that we can offer the best cannabis seed prices available anywhere in the online market, so you ll always be getting the best deal. Step 2 Make a Small Dimple. In fact, when stored under perfect conditions, you can germinate 5 year old cannabis seeds successfully. Source: https://www.taringa.net/Jermaigeahan/proper-storage-and-preservation-methods_5bjcct

This is because baby grass is weak and can t withstand tolerate mesotrione. Origin Jack the Ripper and Orange Velvet. MAC 1 feminized seeds. Source: https://minecraftcommand.science/forum/general/topics/unique-strains-unparalleled-highs

Moisture is one of the three elements required to successfully germinate cannabis seeds ; it essentially helps the seeds to expand and therefore break their shell. Cannabis can freeze or boil to death. This is partly due to the fact that its founder, Robert Bergman, has been growing cannabis for more than 25 years so he knows what people expect. Source: https://py.checkio.org/class/check-for-customer-support-availability/

We offer a wide variety of premium cannabis seeds, including indica, sativa, and hybrid strains. B,C Close-up of clusters of anthers formed within the calyx tissues adjacent to the brown stigmas. Indoors your plants will need a fresh air intake, stale air exhaust and a fan for air movement. Source: https://diveadvisor.com/mohafonroy/germinating-success-tips-on-buying-and-starting-your-weed-seeds

Flavor Chocolate, Citrus, Diesel, Earthy. Of course, these include auto-flowering and feminized seeds, but also regular seeds for advanced growers who want to make their own breeds. Scotts Turf Builder Weed and Feed 3 is a fertilizer and post-emergent herbicide, so it is designed to be used in late Spring when target weeds are young and actively growing. Source: https://wowgilden.net/forum-topic_447118.html

Fill each hole in the seed tray with a peat pellet. This is partly due to the fact that its founder, Robert Bergman, has been growing cannabis for more than 25 years so he knows what people expect. Even a seed that is a few years old can become a thriving plant. Source: https://educatorpages.com/site/alexysstiedemann/pages/consider-feminized-or-auto-flowering-seeds

0 Feb 08, 2021. 99 GBP you spend and an additional 17 off for Bitcoin purchases. Kew Verbena Seeds. Source: https://www.papercall.io/speakers/102425/speaker_talks/264162-organic-seeds-for-natural-cultivation

Well, guess what. We take great pride in all our cannabis seeds and only stock healthy, viable seeds that will produce the most wonderful marijuana plants you can dream of. Our website won t work properly without the assistance of functional cookies; these can t be disabled. Source: https://academicexperts.org/discussions/18807/

The appearance of the seed isn t a reliable indicator of any particular plant quality. Both hemp and cannabis seeds are rich in essential Omega fatty acids. Harshil Landrace Seeds. Source: https://blend.io/post/65b52c92022b4ba9182d1d4c

You can also use the filters in this section to view seeds according to indica sativa balance, predicted height, yield, price, and most importantly in this section climate. If the majority of the pistils have turned from white to brown or orange, it s another indication that the buds are reaching maturity and are ready for flushing. Fill each hole in the seed tray with a peat pellet. Source: https://bhattis.com.pk/the-ultimate-guide-to-buying-and-growing-cannabis-seeds/

We give bonus points to online seed banks that include free seeds with the majority of purchases or offer frequent discounts and specials. Humans, for decades have combined different species from all over the world. That is a large range, but asking how much weed seeds costs is a lot like asking how long a piece of string is. Source: https://tibigame.net/cultivating-bliss-a-guide-to-buying-and-growing-cannabis-seeds_397237.html

Safe and discreet shipping. This topic is discussed further in Keeping New Weedy Invaders Out of the Field. We will keep you informed about the best offers, deals, discounts, blogs, and news. Source: https://sjimera.biz/2024/02/07/from-seed-to-splendor-a-comprehensive-cannabis-cultivation-guide

Generally, the same approach can be applied to Spain as a whole. Twelve hours or more of night will induce flowering. If you have an eye for quality cannabis seed banks, a trusted name, and credibility, ILGM is your go-to brand. Source: https://davinaclaire.com/budding-beginnings-a-comprehensive-cannabis-seed-guide_684853.html

Why does my cannabis plant want to flower in the vegetative stage. When seeds are harvested will affect longevity. We hope you enjoy this fairly new development in cannabis breeding. Source: http://steve-kitchen.tribefarm.net/the-cannabis-enthusiasts-guide-seed-buying-edition/

Scotts Turf Builder Weed and Feed 3 is a fertilizer and post-emergent herbicide, so it is designed to be used in late Spring when target weeds are young and actively growing. Most home growers will never experience an intersex plant if they buy quality feminized seeds and avoid the hype strains that are commonly made from untested elite clones. Step 7 Harvesting, Drying Curing For Best Quality Buds. Source: https://www.bcspir.com/the-ultimate-guide-to-buying-and-growing-cannabis-seeds/

Horsetail Weed Equisetum arvense. Although Quebec Cannabis Seeds lacks the variety of many of the other seed banks on this list, it helps make up for it in a variety of ways namely, fast delivery, awesome discounts, and high-quality seeds. While germination is a natural process, factors such as light, humidity moisture, and temperature must be controlled for cannabis seeds to sprout. Source: https://thecheatersguild.com/2024/02/07/navigating-the-world-of-cannabis-seeds-a-comprehensive-manual

We also have many feminized and autoflower seeds of the Kush strain. Merchandise Total Shipping Charges Up to 19. Summary – Why Choose Seedsman. Source: https://www.wt-berger.at/seeds-of-serenity-a-cannabis-cultivation-adventure/

Best Practices for Feminizing Seeds. Since weed and feed products are designed to prevent germination — or to eradicate a living plant — they can, for the most part, have a similar effect on young turf grass. Buying Cannabis Seeds. Source: https://pixeljoint.com/pixelart/154953.htm

Sonoma Seeds is one of the few online seed banks that ship globally. Many harvest their buds as the trichomes are transitioning from clear to cloudy. Top 5 Seed Banks Online. Source: https://we.riseup.net/jonfllman/expertly-bred-and-tested-genetics

When the branches snap rather than bend it s an indication that the plant is dry enough for curing to begin. Since 2019, we have launched a brand of products rich in CBD Frenchy Flavours. It is almost practically impossible to tell a female or a male marijuana seed just by sight alone. Source: https://fubar.com/bulletins.php?b=2384461127

So, let s get started. Should you wait. Seed Supreme has great customer service, especially when it comes to how fast they respond to your questions. Source: https://imageevent.com/andrewssupreme/gethighyieldsandpotency

Greg – August 20, 2021. Crop King Seeds Best Cannabis Seed Bank for Reputation. The distance over which pollen is dispersed from individual anthers in hermaphroditic flowers is probably limited to a few meters in indoor or outdoor growing facilities, compared to up to 3 5 km from male plants grown under outdoor field conditions, depending on wind speed and direction Small and Antle, 2003. Source: https://tuservermu.com.ve/index.php?topic=63841.0

Water again. sativa is 818 Mb for female plants and 843 Mb for male plants, owing to the larger size of the Y chromosome Sakamoto et al. Unfortunately, you have a 50 50 chance of getting a male plant when growing a plant from a regular seed found in a nug from your last bag of weed. Source: https://niadd.com/article/1174394.html

cite and release in Houston, Dallas, San Antonio, Austin, and residents of Travis County. 80 or less if you dig around in the sales area. Step 3 Place the Cannabis Seed in the Dimple. Source: https://www.goalissimo.org/forum/viewtopic.php?f=11&t=479465

Eliminate stress. Jack Flash 5 Feminized. Autoflower Seeds Vs. Source: [url=https://www.synfig.org/issues/thebuggenie/synfig/issues/6064]https://www.synfig.org/issues/thebuggenie/synfig/issues/6064[/url]

The weeds easily infest thin or patchy areas. Though the company doesn t offer an explicit germination guarantee, customers report a high germination rate. Filling a pot with the chosen soil Making a hole in the soil Transferring the cannabis seed into the pot Covering the newly planted seed with soil. Source: https://blendedlearning.bharatskills.gov.in/mod/forum/discuss.php?d=6976

tadalafil tablets reviews cialis yellow pill tadalafil eg labo

Can You Smoke Weed Seeds. Now you need to move them to the medium in which they will remain for the rest of the growing process. Our top 10 tastiest cannabis strains list displays some of the most tantalising cultivars available, including Fruit Spirit, Fat Banana, and Haze Berry. Source: http://remue-menage.360etmemeplus.org/2013/06/grow-your-greens-the-ins-and-outs-of-cannabis-seed-selection/

B Genious 11. Bitcoin is usually recommended as it s encrypted and untraceable. If so, you can also smoke a small amount for more cerebral daytime energy. Source: https://bollyspice.com/green-magic-a-comprehensive-guide-to-cannabis-seed-buying/

While some strains do well in both settings, others have a clear preference for one over the other. Trichy Dicky. Mechanical management of weeds. Source: https://elearn.kinohimitsu.com/cannabis-cultivation-chronicles-a-seed-to-harvest-guide/

The goal of the vegetative stage is to keep her healthy and allow the plant to grow as big and strong as possible so that she can hold many, many flowers. Review By Melissa Anthony. Tips For You. Source: https://kazeban.biz/2024/02/07/the-green-path-navigating-cannabis-seed-selection-and-growth

Oxygen and carbon dioxide are two of the most major biologically active gases in soil. Indoor growers often use 18-24 hours of daily light whether they are using autoflower seeds or photoperiod feminised cannabis seeds. You can approach germination in multiple ways. Source: https://tibigame.net/cannabis-chronicles-unveiled-the-ultimate-seed-buying-guide_818744.html

Do it frequently enough that you remove the flower heads before they become seed pods. They ranged from landraces Jarilla, Hoa Bac Silver, and Brazil Amazonia , to autoflower strains Northern Lights, Acapulco Gold, and Snow White to commercially grown strains CBD Therapy, Space Queen, Pennywise, Girl Scout Cookie, Copenhagen Kush. If you live in the part of the world where summers tend to be on the longer side, and the sun tends to shine just a few hours more, this period will take more time to finish. Source: https://1buy.today/2024/02/07/mastering-cannabis-cultivation-choosing-and-growing-seeds

Some people like to top remove the growing tip their auto to produce a bushier, shorter plant. Though not as potent as sinsemilla, the remaining flower material can still be potent. Master Kush Automatic. Source: https://davinaclaire.com/cannabis-chronicles-unleashed-the-seed-buying-adventure_418477.html

Mature weeds may require repeated applications for total kill. Some growers still visit their nearest seed shop for the personal touch and advice. Water is sufficient for the first few days. Source: https://speedlliner24.biz/2024/02/07/cultivate-your-oasis-a-guide-to-buying-and-growing-cannabis-seeds

Next, add enough water to make it damp but not soaked. Scanning electron microscopic observations of anthers and pollen grains were made following preparation of the samples according to the procedure described by Punja et al. Cannabis seeds germinate best at a temperature range of 70 – 78 F, and it s recommended to keep your growing environment between 74 – 78 F when germinating cannabis seeds. Source: https://www.steripak.cz/cultivating-green-a-comprehensive-guide-to-cannabis-seed-buying/

Yield 325 – 450 gr m2. latifolia Zizotes milkweed A. The only thing you need for this method is a paper towel, although I would also recommend using two plates. Source: http://mtb.orienteering.de/allgemein/seeds-of-knowledge-a-complete-guide-to-cannabis-cultivation/2013/06/12/

Here are a few things to consider before buying marijuana seeds online. We have one of the most expansive collections of feminized cannabis seeds online. During this stage, you ll want to switch to a nutrient solution high in phosphorus and potassium, as this will help promote bud growth and density. Source: https://getfoureyes.com/s/0G1OI/

This can be avoided by using autoflowering cannabis seeds, as these are not dependent on the season. You can reapply after at least 30 days as long as your turf is listed as safe. This process doesn t change the seed DNA in any way but ensures that all seeds have two X chromosomes. Source: https://www.mrowl.com/post/gettgoepp/playplinko/discreet_and_secure_packaging_options

Based In London, UK. Some, like Brazil, are halfway between legalization and total prohibition, while countries like Uruguay have legalized cannabis in a bid to halt illegal trafficking of the substance. Less dormant seeds of Sinapis arvensis L. Source: https://fubar.com/bulletins.php?b=1738268767

I bet caraway might be a good, close substitute if you just can t get dill seed. Spain is unique in that it operates as a series of decentralised regions, each one capable of making their own regulations in regards to cannabis. Or you could use a readily available container like an empty plastic vitamin jar. Source: https://factr.com/u/fabian-bechtelar/wide-selection-of-top-quality-strains

Purple Queen reigns supreme in the cannabis garden. Cannabis Seeds Regular vs Feminized vs Autoflowering vs CBD. Crossing naturally male cannabis plants with feminized ones should result in a yield of seed-bearing flowers, but the resulting offspring will have the same roughly 55 feminine, 45 masculine ratio as seeds created in the regular way, and there is no real advantage to doing this. Source: https://www.schoolnotes.com/blogs/view/132981

It will give you the best of both worlds boosting your energy while making you feel very relaxed. See some tips on preventing your fields from becoming weed seed airports from GROW here. 14 X Research source Once they sprout and produce leaves, you can decrease the temperature to 70 to 80 degrees Fahrenheit. Source: https://likabout.com/blogs/377530/Competitive-prices-for-top-quality-seeds

Inputs Deposits and Losses Withdrawals. At this point, the seeds will want light, and lots of it. And for the newbies among you – we ll also give you a few tips on how to choose and grow marijuana seeds. Source: https://platform.blocks.ase.ro/blog/index.php?entryid=34005

Some cannabis growers use Rockwool cubes to germinate marijuana seeds. Yes, growing cannabis is legal in 18 US states, as long as you re growing cannabis plants for personal use. When new seeds with exciting novel chemical potencies come in, they have to undergo extensive R D. Source: https://www.hollywoodfringe.org/projects/2125?review_id=43544&tab=reviews

Do cannabis seeds smell. Dormancy is distinguished into two types primary and secondary dormancy Karssen, 1982. Height 55 – 65 cm. Source: https://www.xulas.net/greenhouse-glory-exploring-cannabis-seed-selection-and-growth/

When sowing seeds outdoors, work up the soil in a protected location in early to mid-November. Overwintering butterfly weed is a simple matter of cutting off the plant stem near ground level as soon as the plant succumbs to cold temperatures in the fall or early winter. People originally used it for medicinal purposes, dating as far back as ancient Egypt. Source: http://www.segnidonde.com/2013/06/17/grow-your-greens-the-ins-and-outs-of-cannabis-seed-selection-2/

рейтинг септиков для загородного дома

and Striga gesnerioides Willd. Here are some of the most common questions about cannabis seeds. Your opinion is valuable Please tell us how you plant germinated seeds in the comment section below. Source: https://arespagroup.com/budding-beginnings-a-comprehensive-cannabis-seed-guide/

This will look like a little white tail coming out of the seed. The ideal pH range for cannabis plants is between 6. F Young terminal inflorescence with developing hair-like stigmas. Source: https://none-o-your.biz/2024/02/07/sowing-dreams-a-comprehensive-cannabis-seed-buying-guide

One of the basic principles of cultivating good food crops is the removal of all plants that would compete for space, nutrients, light, and moisture Weeds. Under lights, autos can go from seedling to fully mature plant in as little as 10 weeks. retroflexus, C. Source: https://onsetla.com/2024/02/07/seed-selection-mastery-a-guide-to-cannabis-cultivation

A Feminized seeds are created through a process called feminization. Sign up for our newsletter. Two thousand seeds were buried within a 3 sq ft frame to allow recovery during the course of the experiment. Source: https://apkzilla.info/seeds-of-serenity-a-cannabis-cultivation-adventure_549721.html

What Happens if I Germinate Cannabis Seeds Early. 5 oz or less CBD oil Illegal N N North Dakota Decriminalized 14 g 0. Choose from high CBD strains, autoflower options, and more. Source: http://www.ninedvr.com/9447

Many people are even buying cannabis seeds and growing marijuana on their own. Overall, it is one of the best cannabis seed banks for those looking for high-quality feminized seeds. Cannabis seeds should be stored in a cool, dark place at stable temperatures. Source: http://eothon.vn/green-revolution-a-guide-to-cannabis-seed-purchase-and-growth/

A key benefit of this technique is that your seedlings won t be subject to transplant shock. These go for only 35- 40 for 5 seeds, and you ll get healthy plants with little to no maintenance. Not having to transplant the seed after it sprouts means you don t risk damaging it causing it shock that will slow growth. Source: http://www.illuminareleperiferie.it/2013/06/seed-shopping-101-a-manual-for-cannabis-enthusiasts/

https://bkleon-android.ru/

After 4 – 6 nodes, plants should be producing small 5 bladed leaf sets that will grow to become large fan leaves as the plant develops. 1986 revealed that introduction to the cycle of secondary dormancy in the seeds of A. Easier to grow. Source: https://mumbaimalmo.se/2024/02/07/the-cannabis-enthusiasts-guide-seed-buying-edition/

then take them out and follow the paper towel and plates instructions. There are six systems currently being used on Australian farms and they have been initially developed by farmers. Medical marijuana seeds are designed to produce plants with high CBD levels. Source: http://fedomede.com/2013/06/26/from-seed-to-spliff-a-cannabis-growing-odyssey/

Pumpkin Spice Feminized. Don t expect your high to be clouded by anything else at just 0. E,F Mature anthers that have become dried. Source: https://mybucketpay.com/the-seed-vault-a-journey-into-cannabis-cultivation/

It is undoubtedly among the most prominent strains of this seed bank. Savanna Bous is a digital editorial assistant at Better Homes and Gardens. This also works the opposite way; shorter summers with fewer sun hours create shorter vegetative periods. Source: https://numer-tovar.biz/2024/02/07/seed-sowing-secrets-a-deep-dive-into-cannabis-cultivation

With any of these methods, remember that seeds will need adequate warmth, moisture, and air to germinate properly. Kew Bishop s Weed Seeds. Some of the members of this incredible bank have created Silent Seeds and have joined forces with none other than Sherbinski, the most successful breeder of the last years. Source: https://modyhair.com/seed-shopping-101-a-manual-for-cannabis-enthusiasts_459230.html

Likewise, anyone over the age of 21 can grow up to six plants for personal use in Colorado. Reputable Cannabis Seed Banks in the US Crucial Factors. HPS Or MH For Seedlings. Source: https://biz-igarashi.biz/2024/02/07/budding-beginnings-a-comprehensive-cannabis-seed-guide

Which are the best cannabis seeds for you. Cannabis seeds have an undeniable beauty and appeal. The paper towel method is a favorite for many home growers. Source: https://newiframe.biz/2024/02/07/cannabis-seeds-101-a-comprehensive-buyers-manual

The chemical treatment method involves using silver thiosulfate to feminize a female plant. Gently pinch the seeds to tease them away from the fluffy stuff. However, ILGM and Crop King Seeds tend to have faster and more affordable US delivery times. Source: http://wp-test.belgianmetalshredder.be/2024/02/07/the-cannabis-enthusiasts-guide-seed-buying-edition/

The leaves will be ready to grow and absorb more light which will power future photosynthesis. Higher THC usually does mean more psychoactive effects. With over 30 years experience at the leading edge of cannabis breeding, Dutch Passion has assembled unique seed collections featuring the world s best genetics from dutch original classics to the latest USA flavours. Source: https://www.hackerrank.com/our-selection

While clones and seeds will both do the trick, seeds also seem to be a more popular route in many areas. Davis 2004 recommended the following simple procedure for scouting the weed seed bank. Regular Cannabis Seeds. Source: https://conifer.rhizome.org/Dane6/customize-your-growing-experience

How to use dill seed How to use dill weed. If the pH of the water goes below 5, you will have to discard it and start over, or increase it with pH Up. The planting media should be moist, and loose before placing the seed. Source: https://fubar.com/bulletins.php?b=3336244822

You don t want to overpay for seeds. The three counties that make it up are Mendocino County, Humboldt County, and Trinity County, all of them noted for their production of cannabis. Know the law. Source: https://imageevent.com/andrewssupreme/elevateyourcannabiscultivationgame

Tracking costs extra. Male is a male and a female is a female. There is no need to reduce daily light hours to 12 hours in order to initiate flowering. Source: https://www.adflyforum.com/viewtopic.php?f=35&t=139039

ILGM isn t only about high-quality seeds; they also offer pretty interesting discounts. Review By jean davis. With the Ministry of Cannabis, you can buy a mix of their high-quality weed seeds and have the benefit of trying out different strains – all while saving money. Source: [url=https://linkhay.com/link/7428253/unlock-the-full-potential-of-cultivation]https://linkhay.com/link/7428253/unlock-the-full-potential-of-cultivation[/url]

Pack your soil or other grow medium down around the roots well enough to support the plant while new roots grow, but not so tight that the soil restricts outward root growth. If they have not germinated after two weeks, then they are likely a dud. At harvest time, weeds that have escaped season long management often have mature seed still attached to the parent plants. Source: https://youdontneedwp.com/Nathagrimes/experience-the-art-of-self-sufficiency

This is a sign that the plant is entering dormancy for the season. Feminized Seeds Autoflower Seeds Canada Seed Banks. Top 10 Cannabis Seed Banks To Buy Cannabis Seeds Online. Source: https://blendedlearning.bharatskills.gov.in/mod/forum/discuss.php?d=7031

Example On a 100 pre-tax purchase with a 20x bonus multiplier a Member would earn a bonus 8 in CT Money 20 X. These exclusive cannabis seeds represent our latest work. Save preferences Refuse Cookies. Source: https://koreanstudies.com/forum/viewtopic.php?t=1003

While not as impressive, we also offer Green Crack autoflower seeds, if you don t care as much about the sights of tall trees and just want to try her amazing, uplifting buds as soon as possible. What Are the Best Seed Banks in 2023. In order to grow at its best and give you the juicy buds, you love cannabis requires some fundamental things. Source: [url=https://www.micromentor.org/question/17445]https://www.micromentor.org/question/17445[/url]

This plant is essential to the life cycle of monarch butterflies because the insects need milkweed to lay their eggs. Crop residue management. As you know, ILGM is famous for its Buy 10 Get 10 Free deals. Source: https://platimzafoto.ru/sowing-success-a-journey-into-cannabis-seed-selection/

https://calculatortiktok.com/

https://bk-leon-skachat.ru/

Mimosa Clementine X Purple Punch X Auto Purple Punch. The okra tasted good after about six weeks, though it clearly did not have the dill pickle taste I love from the jar. All you have to do is place your seed carefully in your seed plug and follow the instructions when watering; different brands and models have different watering instructions. Source: https://gpniko.ru/seeds-of-serenity-a-cannabis-cultivation-adventure/

The importance of shallow tillage as a weed control method in the false seedbed technique has also been highlighted. For Autos they will flower when ready or mature enough hense the Auto then you can switch to red or a combination of red and blue light all the way through until harvest. This helps the weed survive in a periodically disturbed, inhospitable, and unpredictable environment. Source: https://aldizkaria.biz/2024/02/07/embark-on-greenery-buying-and-growing-cannabis-seeds-demystified

While temperature first catalyzes the chemical reactions that take place, moisture allows the seed embryos to grow and expand, eventually breaking the seed shell to sprout into a seedling. You can make a peroxide solution for soaking seeds by combining 1 part household peroxide 3 with 3 parts tap water. Just pick your favorite strain, put them in your shopping cart, and we will make sure you have the grow of a lifetime. Source: https://rimteramo.biz/article/2024/02/07/greener-pastures-your-ultimate-guide-to-cannabis-seed-buying

Education is a huge part of what Homegrown Cannabis Co. The third type of weed, bittersweet nightshade, is one of the most poisonous plants, despite being related to the tomato. Strains like the legendary Chemdog wouldn t be possible without adventurous smokers planting and proliferating the seeds they found in a bag. Source: https://livewirerecordings.net/2024/02/07/the-ultimate-guide-to-buying-and-growing-cannabis-seeds

Like most living creatures such as humans, animals, and other plants, the cannabis plant also has male and female genders and reproductive systems. Even though they both come from the same plant, dill seed and dill weed have vastly different flavors. Hydroponic systems offer the advantage of year-round cultivation and the ability to grow plants in various locations. Source: http://www.spurcrossbnb.com/?p=18382

The main drawback is a lower success rate. язык можно изменить в настройках аккаунта. The foil will act like a small greenhouse, keeping the inside of your pot warm and moist. Source: https://gameformobi.com/sowing-dreams-a-comprehensive-cannabis-seed-buying-guide_609993.html

5 oz 14 g ; first or second offense only. Don t be afraid to scarify. Last but not least, Gelato feminized cannabis seeds are available on the famous Seed Supreme a long-standing company with a reputation for seed variety and free shipping over 90. Source: https://gigspeeddev.biz/2024/02/07/sowing-dreams-a-comprehensive-cannabis-seed-buying-guide

This attention to the freshness of their seed supply helps make Ministry of Cannabis one of the most reliable seed banks out there. CRITICAL KUSH AUTO. Ideally a sturdier stem is better. Source: https://www.proiectarges.ro/cannabis-chronicles-unleashed-the-seed-buying-adventure/

Free shipping on all orders Shop now. This can be prevented by removing the seed pods before they dry and burst open. 5 centimeters 0. Source: https://www.hackerrank.com/expertly-grown-and-harvested-seeds

Here are some of the most common questions about cannabis seeds. After amplification, each PCR reaction was subjected to electrophoresis on a 1. These hermaphroditic plants often develop due to environmental stressors, including inhospitable weather and nutritional deficiencies. Source: https://exchange.prx.org/series/46624-superior-genetics-for-optimal-growth

She founded Gaia s Farm and Gardens, a working sustainable permaculture farm, and writes for Gaia Grows, a local newspaper column. The datasheet will tell you the exact ratio of genetics for example 50 sativa, 50 indica. Lightproof pot or mug. Source: https://minecraftcommand.science/forum/general/topics/find-the-perfect-strain-for-you

That said, they re known to send free seeds on every order, even though they don t advertise it. This initial, or primary, dormancy delays emergence until near the beginning of the next growing season late spring for warm-season weeds dormancy broken by cold period over winter , and fall for winter annual weeds dormancy broken by hot period in summer when emerging weeds have the greatest likelihood of completing their life cycles and setting the next generation of seed. Water Your Soil Well. Source: https://foodle.pro/post/60492

If a significant weed seed rain has occurred, leave weed seeds at the surface for a period of time before tilling to maximize weed seed predation. 5 cm deep into each pellet. This is another easy method, but it does require transplanting the seeds once they have sprouted. Source: https://wowgilden.net/forum-topic_447317.html

tadalafil generique cialis tadalafil peptide dosage cialis prices cvs

Greetings from California! I’m bored to tears at work so I

decided to check out your website on my iphone during

lunch break. I really like the knowledge you present here

and can’t wait to take a look when I get home. I’m amazed at how fast your blog loaded on my phone ..

I’m not even using WIFI, just 3G .. Anyways, excellent blog!

I saw similar here: Sklep online

Как выбрать лучший рулонный газон для климата вашего региона

рулонный газон стоимость https://rulonnyygazon177.ru/ .

You usually do not need to wait longer than ten days. The plant should grow great indoors or outdoors, depending on the cultivation space available. The float test. Source: https://www.findit.com/wzpwcongybpvcnn/RightNow/in-the-realm-of-cannabis-cultivation-superior-genetics/85df7e73-8017-4142-b67a-a9d470d95b75

Shallow soil disturbance during periods of peak potential germination can be an effective tactic for debiting drawing down the weed seed bank Egley, 1986. Compound Genetics Total Eclipse Gastro Pop Collection Feminised Cannabis Seeds. Cut the stems long, choosing flowers that have just opened. Source: https://webanketa.com/forms/6gs30e9m68qp4c9n65h3crsm/

Hey superb blog! Does running a blog such as this take a large amount of work?

I’ve very little expertise in programming however I had been hoping to start

my own blog soon. Anyhow, if you have any ideas or techniques for new blog owners please share.

I know this is off subject but I just needed to ask.

Appreciate it! I saw similar here: Sklep internetowy

Thus organic farmers strive both to prevent heavy deposits through propagation of existing weeds, and to prevent establishment of new weed species by excluding their seed and promptly eradicating new invaders. Flavor Citrus, Earthy, Pine, Pungent. Yes, marijuana seed banks are reliable , at least the ones mentioned in this article. Source: http://www.orangepi.org/orangepibbsen/forum.php?mod=viewthread&tid=148881

In short, these are the best feminized cannabis seeds overall because of their combination of high THC potency, good genetics, and ideal growing potential. It has nothing to do with seeding, hence the word established. Free shipping on all orders Shop now. Source: https://koreanstudies.com/forum/viewtopic.php?t=1029

Even then, they still need a lot of light to start flowering properly. Generally speaking, the purchase of cannabis seeds as a collector s item or for purposes other than growing is seen as legal. If you are using a pencil, an easy way to measure is by making a tiny hole as deep as the eraser. Source: [url=http://bonco.com.sg/seedling-success-a-journey-into-buying-and-growing-cannabis-seeds/]http://bonco.com.sg/seedling-success-a-journey-into-buying-and-growing-cannabis-seeds/[/url]

btc price prediction coincodex

You ll need to stratify your seeds, meaning expose them to cold temperatures for a period of time before they ll sprout. Cannabis breeders may cross specific cannabis genetics to produce a strain with all their desirable qualities. A marijuana seed bank , also called a cannabis seed bank, is an institution that is in charge of studying marijuana plants, and also deals with their production and their commercialization. Source: https://daltongrows.biz/2024/02/07/the-ultimate-guide-to-buying-and-growing-cannabis-seeds

Feminized Autoflower High CBD Fast Growing High THC Low THC High Yield Fast Flowering Indoor Outdoor Greenhouse Beginner. A website with numerous customer reviews, and positive ones at that, are more likely to provide you with quality seeds and an overall positive experience. Best Cannabis Seed Banks Conclusion. Source: https://kissmp3.biz/2024/02/07/the-seed-vault-a-journey-into-cannabis-cultivation

Amsterdam Marijuana Seeds insists on having top-notch quality. In rare cases two out of 1,000 plants , the entire female inflorescence was displaced by large numbers of clusters of anthers instead of pistils Figure 3. Considered by many to be the motherland of cannabis in Europe, it s no surprise that cannabis seeds and CBD are legal to purchase. Source: https://stellaletter.biz/2024/02/07/seeds-of-serenity-a-cannabis-cultivation-adventure

Small Plants With Big Yields. Note Many germinate cannabis seeds using a wet paper towel on a plate. Cannabis has never been more popular in the United States, with an overwhelming number of Americans expressing support for legalization, according to the Pew Research Center. Source: http://www.asinaorme.com/2024/02/07/cultivate-your-green-thumb-buying-and-growing-cannabis-seeds/

Outdoors, feminised strains sense the shortened daylight hours as autumn fall approaches and bloom begins. We also understand that this is not always possible, especially when you buy cannabis seeds in the sale. You might even be a customer of a lawn care company but assume that you can still do some of your own seeding. Source: https://doska-ua.biz/2024/02/07/the-seed-vault-a-journey-into-cannabis-cultivation

Some cannabis growers prefer it because it is environmentally friendly. Sensi 1318 CBD. This is a great time to apply new grass seed and choke out the weeds. Source: http://krynicabursztynek.pl/cultivating-cannabis-a-seed-buying-expedition/

Homegrown Cannabis Co. Well, the best is subjective but we really like Lambs Breath. Clones are also subject to pesticide screening in accordance with state regulations. Source: http://sw16.co.uk/from-seed-to-smoke-a-cannabis-seed-buying-extravaganza/

Protective Shield fits over weeds to contain spray and help protect desirable plants Use in and around vegetable gardens, flower beds, tree rings and mulched beds, as well as on cracks. MSNL Seedbank Best For Quickest Delivery. When can Cannabis be Harvested Outdoors. Source: https://www.oxox.co.jp/2013/12/30/the-seed-vault-a-journey-into-cannabis-cultivation/

, 2005; Schutte et al. incarnata Common milkweed A. Now That You Know How Easy It Is To Grow Cannabis, Pick A Strain. Source: http://molbiol.ru/forums/index.php?showtopic=1078071

Клиника СВЕТОДАР оказывает широкий спектр офтальмологических услуг и заботится о потребностях пациентов. Стремимся учесть их пожелания, чтобы лечение было комфортным и действенным. Персонал центра состоит из грамотных специалистов, вы можете легко доверить заботу о своих глазах. https://sp.svetodar.pro/ – сайт, где вы сможете получить нужную информацию о клинике. Здесь можно ознакомиться со списком предоставляемых услуг и отзывами пациентов. Мы постоянно работаем над повышением качества сервиса.

You can shop by flowering type, with countless feminized seeds, autoflowering seeds, regular seeds, and more. This means you won t have any veg time at all if you grow outdoors. Thanks again, and I hope you continue to enjoy the blog. Source: https://pledgeit.org/consistent-reliable-germination-rates

מחכות לך כמה נערות מהממות, הן זמינות בשבילך ביום ובלילה גם בסופי שבוע, תרגיש חופשי להתקשר אליהן ולשאול פרטים על השירות שלהן. להרפות ולהתמקד בהנאה המינית שלכם. זה עוזר לשחרר מתח ומקדם תחושה עמוקה יותר של מיניות, מתן בריחה נחוצה מאוד מן הדרישות של העולם נערות ליווי בחיפה

High CBD low THC strains such as CBD Charlotte s Angel or CBD Auto Blackberry Kush won t get you high since THC is present at very low levels. Over 95 of people that grow from cannabis seed use feminised seeds or autoflowering seeds. Understanding the fundamentals of cannabis growing is a good place to start your marijuana growing journey. Source: http://www.fanart-central.net/user/Cathy46/blogs/20749/Discover-our-premium-cannabis-seed-selection

Thought to be descended from either Zacatecas Purple an original Mexican sativa landrace or Afghani Skunk, the strain features about 70 sativa content with maximum THC levels clocking in at about 25 per dry weight. It can take up to four weeks for the herbicide effective to fade, so sowing grass soon after applying weed and feed is likely futile because new grass won t be able to grow. The widespread availability of high quality marihuana seeds allowed an explosion of small- scale growing. Source: https://linkhay.com/link/7429637/start-your-next-grow-journey

Opposite-Leaved Saltwort Barba Di Frate Salsola soda. If you re looking for something mild and herbal, dill weed is the right choice for you. In addition, you only need to spend 90 to get free shipping , which is the lowest threshold you will find in most seed banks excluding ILGM. Source: http://hungryforhits.com/myprofile.php?uid=34555&postid=17935

We are actively responding to the vast amount of emails and Dm s that come our way. The hybrid of Big Bud and Purple Urkle is a great sleeping aid , as well as a euphoria booster. Wish me luck as I think I m going to need it. Source: https://jobhop.co.uk/blog/294651/trusted-and-experienced-seed-banks

uk 024 7630 3517. 8 percent Minimum order of 70 10 standard shipping option only The website is basic with few additional details. To eat them as food they contain a lot of omega 3 and omega 6. Source: https://www.micromentor.org/question/17447

שמפרסמות את עצמן באתר רוצות לתת לך תחושות הכי מאושרות, אימוץ מושג ההנאה החושית ומציעות תפריט נרחב של שירותי . הן בכיף מבטיחות לך אינטימי איכותי משמש במשך מאות שנים לקידום רווחה פיזית ורגשית. גאות להציע אווירה בטוחה, נקייה ונעימה עבור לקוחותיהן. נערות הכי דירות דיסקרטיות באשדוד

Because they have grown up in their surroundings, they will have acclimated to them. How is cannabis able to flower automatically. Edit business info. Source: http://www.associationheroux.ca/the-green-path-navigating-cannabis-seed-selection-and-growth/

Some can live for decades. A good example is broccoli, which is the very same species of plant as cabbage, cauliflower, Brussels sprouts, kale, and kohlrabi. was 40 higher as compared to the corresponding value recorded for winter annuals Hirschfeldia incana L. Source: https://bizkaikotxapelketa.biz/2024/02/07/from-seed-to-smoke-a-cannabis-seed-buying-extravaganza

Growing great buds in a spare cupboard. To ensure a good crop, you ll want to germinate and plant many marijuana seeds and then separate the females from the males when the plants begin to show their sexuality. californica Desert milkweed A. Source: https://fk-vizit.ru/2024/02/07/green-revolution-a-guide-to-cannabis-seed-purchase-and-growth

Should I Apply Weed and Feed or Seed First. The cultivation of cannabis for personal consumption is an activity subject to legal restrictions that vary from state to state. Ideally, you should plant seeds well enough before frost in the autumn so that the new grass will grow for several weeks before sleep. Source: https://finnlore.de/2024/02/07/from-seedlings-to-splendor-your-cannabis-seed-buying-journey

עם גירוי אירוטי ויוצר חוויה ייחודית החורגת מבילוי מסורתי. המטרה העיקרית של היא לעורר את החושים, לשחרר מתח ולקדם את הרווחה אנדורפינים מפגש איכותי עם צעירות הסקסיות ביותר של מתחיל בדרך כלל בהתייעצות קצרה בטלפון. במהלך השיחה שואלים אותך על העדיפויות או נערות ליווי בתל אביב

Equally, buying cannabis seeds from reputable stores like Herbies ensures that you purchase from diversified, reliable supply chains, keeping the cost reasonable. When to Apply Weed and Feed. Curly Dock Rumex crispus. Source: http://sanpedroitza.com/seedling-symphony-a-guide-to-cannabis-cultivation-mastery/

Because Silent Seeds and French rapper Duc have achieved something no one has ever done before a THC generation of 32. However, once germinated, cannabis seeds become illegal in many countries. The best ones acknowledge that this can happen and take steps to remedy any issues customers have. Source: https://onsetla.com/2024/02/07/green-dreams-a-journey-into-cannabis-seed-acquisition

Ahora, sabras distinguir entre marihuana macho y hembra con la ayuda que te traemos, ya que es algo realmente sencillo, pero que si no se explica bien puede llegar a ser algo lioso. DNA Extraction, PCR, and Sequencing. Hermaphrodite Plants These plants have both the stigmas and pollen sacs in their nodes. Source: https://www.arjunabikes.cl/?p=13235

Flavor Citrus, Pine, Pungent, Skunk. Feminized Autoflower CBD Fast Version High THC High Yield Indoor Outdoor Beginner Mix Packs. The Possible Effects of Light, Gaseous Environment of the Soil, Soil Nitrates Content and Soil PH on Seed Germination of Various Weed Species. Source: https://youroptionsmobile.com/2013/12/30/seedling-symphony-a-guide-to-cannabis-cultivation-mastery/

Свартехкомлект предлагает сварочные материалы и оборудование по наилучшим ценам. У нас имеются в наличии выпрямители, инверторы, трансформаторы, горелки, генераторы, реостаты, резаки и многое другое. Квалифицированные специалисты помогут вам с подбором, они быстро обрабатывают заявки. https://www.svartk.ru/ – сайт, где представлен богатый выбор расходных материалов для сварки. Гарантируется доставка в короткие сроки. Решив купить у нас сварочное оборудование, можете не сомневаться в результативности выполненных работ.

Cannabis Seeds are restricted by law to 25 seeds per order. Mary Jane s Garden – Weed Seeds for Sale Straight From the Source. Contact Details. Source: https://conifer.rhizome.org/Dane6/affordable-prices-for-top-genetics

The sizes of the PCR products were compared with a molecular size standard 1 kb plus DNA ladder. Most orders ship within 2 business days. To do this, germinate your cannabis seeds in a glass of water. Source: https://topgradeapp.com/lesson/expertly-grown-and-harvested-seeds

And, I must not forget to mention, these autoflower marijuana seeds are all feminized, ensuring that your plants will be exclusively female, exploding into flower after just 2 to 4 weeks of initial growth. Seed City Cheap Cannabis Seeds for Sale. While these fungi can lie dormant in soil, they grow and thrive in overly wet conditions. Source: https://original.misterpoll.com/forums/1/topics/344692

Evaluating the Weed Seed Bank. Your plant will be ready to be harvested once flowers are compact and the pistils turn orange brown. The stem could bend and not develop properly, and the roots might sprout upward. Source: https://www.surveyrock.com/ts/DRNR5Q

Free cannabis seed s from 25 25 off Kera seeds currently 30 off a variety of seeds and regular free seed giveaways. Plants need nurturing for months in the right environment with a close eye for detail. Individual clusters of anthers were carefully removed with a pair of forceps and brought to the laboratory for microscopic examination for the presence of pollen grains and for DNA extraction. Source: https://www.findit.com/wzpwcongybpvcnn/RightNow/one-invaluable-resource-to-aid-in-your-search-for-a/0bd77187-8a1e-40f9-bbc0-8fc6426f4b8b

4 nmol seed 1 for applied NO 3 – concentrations between 2. ILGM s strain stock stacks up to 80 different strains. Different color plant tags can be used to identify different strains. Source: https://www.goalissimo.org/forum/viewtopic.php?f=11&t=482347

pontoon boat rentals homosassa fl https://boatrent.shop/

Sign up to our newsletter. Unfortunately, there s not much truth to any of these interpretations. Additional shipping charges Some cannabis seeds aren t cheap. Source: http://forums.hentai-foundry.com/viewtopic.php?t=84099

Can You Smoke Weed Seeds. Your second leaves to emerge will be single blades and will be serrated, looking like regular pot leaves. It will kill most types of weeds. Source: [url=http://gotinstrumentals.com/front/beats/beatsingle/5f2672da-08dd-11e1-b7cb-6bfdb58faeb9]http://gotinstrumentals.com/front/beats/beatsingle/5f2672da-08dd-11e1-b7cb-6bfdb58faeb9[/url]

To determine if a cannabis seed bank is worth buying from, there are a number of factors that you must consider before making a purchase. However, dormancy is not permanent and seeds of many weed species change from a state of dormancy to non-dormancy. The seedling needs little water and minimal nutrients. Source: https://pixeljoint.com/pixelart/154950.htm

Whilst there is not quite the same enthusiasm towards these as there perhaps once was, Seed City is always very proud to offer any regular cannabis strain that is made available to us. Mother s Finest. One company sells motivational speeches delivered by a person who travels by bicycle. Source: https://exchange.prx.org/series/46425-buy-weed-seeds-online-the-ultimate-guide-to-find

You might also want to use their germination guides if you need a hand through the process. What type of Cannabis Seeds does Buds Roses sell. Most outdoor growers plant seeds in early spring, once the threat of frost is gone. Source: https://www.bigoven.com/recipe/420-seeds-cocktail/3073012

Хотите недорого приобрести чемодан на колесах? FEELWAY вам в этом поможет. Предоставляемые нами чемоданы изготовлены качественно, у них крепкие колеса и хорошие молнии, они создают настроение отпуска. Кодовый замок легко настраивается. Приобретением вы точно останетесь довольны. https://feelway.ru/ – сайт, где можно узнать, из чего выполнен чемодан. Также здесь вы можете проверить подлинность товара. Просто введите ваш email, код изделия и нажмите на специальную кнопку «Отправить». Мы вас обязательно проконсультируем, обращайтесь!

cialis levitra generico tadalafil orion tadalafil teva dawkowanie

להשוואה! עם הבחורות הסקסיות שניתן למצוא כאן וטכניקות המפנקות שלהן, חוויה אינטימית זו חייבת לשלוח אותך לעולם של אושר טהור. מומלץ האירוטיות בתוך הפרט ומגבירות את החשק המיני והתשוקה האינטימית שלך. מזמינות גברים מקומיים לביקורים אירוטיים 24/7. חייגו עכשיו דירות דיסקרטיות באשקלון

Провести время интересно можно всегда на сайте Smotret.net, именно здесь представлены достойные сериалы. Расположитесь с комфортом на диване и смотрите с удовольствием. https://smotret.net/ – сайт, который предлагает расслабиться и отдохнуть, тут есть широкая коллекция отменных и качественных сериалов. Смотреть их можно в любое время. Гарантируем, что вас ждет множество занимательных историй. Также предлагается отличная возможность давать свои комментарии к сериалам. Приятного вам времяпрепровождения!

אינטימי איכותי משמש במשך מאות שנים לקידום רווחה פיזית ורגשית. גאות להציע אווירה בטוחה, נקייה ונעימה עבור לקוחותיהן. נערות הכי כשמדובר בהזמנה לביתך או מלון. תקשורת אדיבה וברורה, כבוד והסכמה הדדית הם תמיד חיוניים לפגישות בטוחות ומהנות. חשוב לזכור שצריך דירות דיסקרטיות בבאר שבע

Step 7 Harvesting, Drying Curing For Best Quality Buds. Feminized cannabis seeds are exactly what they sound like cannabis seeds that give only female plants. When your seedling comes above ground, it is going to want to see a direct light source. Source: https://poematrix.com/autores/marquis33/poemas/buy-weed-seeds-best-place-find-and-purchase-high-quality-cannabis-seeds

Pot seeds tend to have a darker color, in tones of black, red, brown, or gray. Banana Kush Cake Feminized. »здели¤, изготовленные Р·Р° пределами вЂ”РЋС Рё попадающие РїРѕРґ действие «акона Рѕ тарифах вЂ”РЋС Рё св¤занных СЃ РЅРёРј законов Рѕ запрещении принудительного труда. Source: https://4portfolio.ru/user/andrewsuplinks-gmail-com/buy-the-highest-quality-cannabis-seeds-online

International law does take precedence over national law, meaning cannabis seeds are technically legal in all of the member states. Sonoma Seeds is a Canadian seed bank that has been in the industry for more than 15 years. As the buyer or owner of said seeds, you are liable for any fines or penalties that may accompany such attention. Source: https://niadd.com/article/1169292.html

This process allows the bud to further dry while breaking down chlorophyll and preserving terpenes and cannabinoids all of which maximize flavour and aroma. However, confining weed management to a narrow temporal window increases the risk of unsatisfactory weed management due to unfavorable weather Gunsolus and Buhler, 1999. An honest guide to buying cannabis seeds saving money. Source: http://forum.amzgame.com/thread/detail?id=270697

First, consider how the methods used in this experiment might influence the results. However, humidity ranging from 9 20 may also cause a myriad of issues such as insects, fungi, and even seed sweating due to excessive heat. What exactly is the difference. Source: https://pixeljoint.com/pixelart/154708.htm

Alternatively, use the RQS Autoflowering or Feminized Starter Kits to provide your seeds with the perfect conditions from the get-go. Growing Male and Female Plants. Summary – Why Choose Seedsman. Source: https://blendedlearning.bharatskills.gov.in/mod/forum/discuss.php?d=6651

Sow seeds directly in the garden butterfly weed does not require much tending to in order to thrive, Water a new plant well during its first growing season but the plant will prosper even in drought-like conditions when established. Culinary Use. If you re growing cannabis outdoors, harvest time will also be dictated by the season. Source: http://www.studentsreview.com/viewprofile.php3?k=1143046560&u=580

Once you buy the seeds, you never really know what you re going to get until you ve grown the plants. Let s explore these now. Plant sprayer. Source: http://ongzx.com/cannabis-connoisseurs-guide-the-seed-buying-edition/

Популярная компания FARBWOOD предлагает купить продукцию из лиственницы в Минске по привлекательной стоимости. В работе своей используем только современное оборудование, гарантируем выгодные скидки, широкий ассортимент изделий, быструю доставку и высокое качество. farbwood.by – https://farbwood.by/сайт, где имеется возможность детальнее посмотреть условия доставки и оплаты. Также здесь имеется каталог, представлена галерея и контактная информация. Позвоните нам, мы проконсультируем по каждому товару либо по услуге.

Plants react to the low fidelity between germination cues and recruitment potential and have become able to produce seed populations with different germination demands not only in qualitative but also in quantitative points to secure the longevity of the population. Regarding the winter annual S. At this stage you can drop your blue light down to 46 60 cm from the cotyledon depending on the light you are using. Source: https://picquick.ru/the-art-of-cannabis-gardening-seed-selection-and-cultivation/

Howdy! Do you know if they make any plugins to help with SEO?

I’m trying to get my blog to rank for some targeted keywords

but I’m not seeing very good gains. If you know of any please share.

Thanks! You can read similar article here: Sklep online

As the leaves of the plant get bigger, they can gradually handle more sunlight, so move it into more direct light– the more light the better. Nevertheless, several states continue to seize shipments that they are aware contain marijuana seeds. Everyone has different preferences that come into play. Source: https://orangegoldgym39.ru/2024/02/07/cultivate-your-green-thumb-buying-and-growing-cannabis-seeds

There are both male and female seeds. Equisetum hyemale , by contrast, is a more useful horsetail plant to the landscaper. Therefore, skunk with a high content of CBD is particularly suitable for people who have therapeutic purposes for it. Source: https://iugansk.ru/2024/02/07/seed-shopping-101-a-manual-for-cannabis-enthusiasts

The dishes here start from the ground with this celeriac katsu in the roots and bulbs section of the menu. One is that the cubes are cheap and easy to find. But that doesn t mean compromising on quality. Source: https://stocktontrain.net/2024/02/07/navigating-the-world-of-cannabis-seeds-a-comprehensive-manual

X-Seed liquid for an hour. PMID 9846457. Chances are that Seedsman has it. Source: https://www.arjunabikes.cl/?p=13237

Das Zet Casino Forum: Alles, was du wissen musst

Das Zet Casino bietet seinen Spielern nicht nur eine Vielzahl von spannenden Spielen, sondern auch die Möglichkeit, sich mit anderen Spielern auszutauschen und zu vernetzen. Dafür gibt es das Zet Casino Forum, in dem Spieler ihre Erfahrungen teilen, Tipps und Tricks austauschen und sich über aktuelle Aktionen und Angebote informieren können.

Im Zet Casino Forum findest du verschiedene Bereiche, die auf unterschiedliche Themen rund um das Casino-Spiel spezialisiert sind. So gibt es beispielsweise Abschnitte für Strategien und Taktiken, wo Spieler ihre besten Tipps für bestimmte Spiele wie Roulette, Blackjack oder Spielautomaten teilen können. Auch gibt es einen Bereich für Neuigkeiten und Ankündigungen, in dem das Casino über aktuelle Aktionen informiert.

Ein weiterer wichtiger Bereich im Zet Casino Forum ist der Support-Bereich. Hier können Spieler Fragen stellen oder Probleme melden und erhalten schnell und unkompliziert Hilfe von anderen Spielern oder den Mitarbeitern des Casinos. So wird eine positive und unterstützende Community geschaffen, die es den Spielern ermöglicht, ihr Spielerlebnis zu maximieren.

Das Zet Casino Forum ist nicht nur eine Plattform zum Austausch, sondern auch eine Möglichkeit, Belohnungen zu erhalten. Durch aktive Teilnahme am Forum und das Teilen von hilfreichen Beiträgen können Spieler Punkte sammeln und diese gegen attraktive Preise eintauschen.

Insgesamt bietet das Zet Casino Forum eine tolle Möglichkeit, sich mit anderen Spielern zu vernetzen, sein Wissen zu erweitern und von den Erfahrungen anderer zu profitieren. Wer also gerne in einer Community von Gleichgesinnten aktiv ist und sein Casino-Erlebnis noch spannender gestalten möchte, sollte unbedingt einen Blick ins Zet Casino Forum werfen.

https://zetcasino.one/

Das Tipico Live Casino ist eine beliebte Plattform für Casino-Enthusiasten, die gerne in Echtzeit gegen echte Dealer spielen möchten. Um bei Tipico Live Casino einzahlen zu können, sollten Sie zunächst ein Konto bei Tipico erstellen. Dies ist ein einfacher Prozess, bei dem Sie persönliche Daten wie Ihren Namen, Ihre Adresse und Ihre Telefonnummer angeben müssen.

Nachdem Sie ein Konto erstellt haben, können Sie Geld auf Ihr Tipico-Konto einzahlen, um in das Live Casino zu gelangen. Es gibt mehrere Zahlungsmethoden, die von Tipico akzeptiert werden, darunter Kreditkarten, Debitkarten, E-Wallets und Banküberweisungen. Wählen Sie einfach die für Sie bevorzugte Zahlungsmethode aus und geben Sie den Betrag ein, den Sie einzahlen möchten.

Sobald das Geld auf Ihrem Tipico-Konto gutgeschrieben wurde, können Sie es im Live Casino verwenden, um verschiedene Spiele wie Roulette, Blackjack, Poker und Baccarat zu spielen. Die Live-Dealer-Spiele bieten eine realistische Casino-Erfahrung, da Sie mit echten Dealern interagieren können, die die Karten mischen und die Räder drehen.

Es ist wichtig zu beachten, dass das Spielen im Live Casino mit echtem Geld Risiken birgt und verantwortungsbewusstes Spielen immer an erster Stelle stehen sollte. Spielen Sie niemals mit Geld, das Sie sich nicht leisten können zu verlieren, und setzen Sie sich ein Budget, das Sie einhalten können.

Insgesamt ist das Tipico Live Casino eine spannende Plattform für Casino-Spieler, die gerne in Echtzeit gegen echte Dealer antreten möchten. Mit einer einfachen Einzahlung können Sie in kürzester Zeit in die Welt des Live-Casinos eintauchen und ein aufregendes Spielerlebnis genießen.

https://tipicocasino.one/